Performance Marketing Reboot - 12.18.24

A Marketing Newsletter for Performance Marketers Converting to Marketers™

Hi Folks,

Squeezing one last newsletter in before the holiday break - my Christmas gift to you all. I’ve intentionally kept this month’s post fairly devoid of holiday/BFCM insights since I have personally seen and heard enough! I also don’t think anything particularly interesting or new happened this year. Consumers were choosy, BFCM broke records, the short Thanksgiving to Christmas period made for trying times etc etc… Every year, I come back to these four, timeless adages:

Q4 is won in Q1 and Q2 (and the prior year) - Plan accordingly in 2025.

Simple, CLEAR, impactful offers only - don’t confuse consumers.

Start Early - if only just to understand what you are up against and adapt.

Embrace the season - lean into seasonal elements, activations.

Now onto the core topics…

Highlights:

Should you be divesting from PMAX?

Proof that Google is used mostly for navigation vs. discovery

eCommerce might finally be back to “normal” times

Performance Media is OPEX (and retail media is a fulfillment cost)

Test I’m Excited About:

What is going on at Google with PMAX and shopping? Back in October, Google announced that PMAX would no longer take SERP priority over standard shopping.

Just a few weeks ago, Google also made clear they are placing a bigger bet on Demand Gen, deprecating video action (VAC) in favor of the ad product that also serves on Gmail and Discover placements and allows for static assets. This sounds like a PMAX redo, more focused on demand generation than demand capture (and also sounds a lot like Meta’s ASC).

Is PMAX going the way of exact match? Or settling in as a more niche part of the Google portfolio instead of the flagship product?

Since its rollout in 2020/2021, PMAX delivered outsized returns for nearly all of our clients. Driven largely by a stark CPC advantage, PMAX offered scale that shopping could not. We rotated much of our portfolio heavily into PMAX and pushed the limits of experimentation for a continued edge. But in late 2023 and early 2024, we started to see that edge disappear. The CPC gap largely disappeared, and campaign volatility gave our team and clients consistent, unexplained headaches.

Over the last 6-12 months, we have resumed more active testing of PMAX vs. Standard Shopping. The below outcomes are from three of our largest Google spending clients and start to explain why Google may be making the changes noted above:

Brand 1 Test: Shopping 2x more incremental than PMAX (geo-holdout)

Brand 2 Test: PMAX 0-10% performance advantage, but too volatile for the brand’s tolerance

Brand 3 Test: Shopping beat PMAX in a UI-experiment

Our overall portoflio trend tells this story clearly. Standard Shopping spend has 7-10x’d since bottoming out in 2023:

We have a number of major tests lined up for Q1 to validate the right campaign investment strategy across the rest of our clients.

Three potential hypotheses as to what happened here:

Google wanted PMAX to bridge demand creation and high intent, demand capture. Doing both at the same time, while operating off one conversion signal, is potentially impossible (at least under current constraints).

Google’s biggest customers did not like relinquishing control and visibility to the algorithm, and reminded Google of this often. Ad dollars may have shifted as a result of this.

Google’s biggest customers have more siloed media teams - search and video teams aren’t necessarily connected and aren’t necessarily goaled the same way, so campaigns that combimed search/PLA’s and video were challenged by this model.

Remember that Google is accountable first and foremost to their shareholders, so whatever the reason, it’s likely it still comes down to ROI for them.

So what can you do? Test Standard Shopping vs. PMAX ASAP. A few considerations:

It’s important to test this for your business - we have seen varied results, and some instances where pmax still outperforms standard shopping.

It’s important to set it up as a lift study - incrementality can vary across the two campaign types.

It’s all likely to keep changing - this test should get you through the next 6-12 months, but its important to retest these variables on a consistent basis given the rate of change in both the ad products and your business.

So what’s next for PMAX? I don’t think its going away. The product still provides value for many small to mid market businesses who rely more on automation and time saving features. And perhaps this is just a short setback in the long journey to complete automation.

Post I Like:

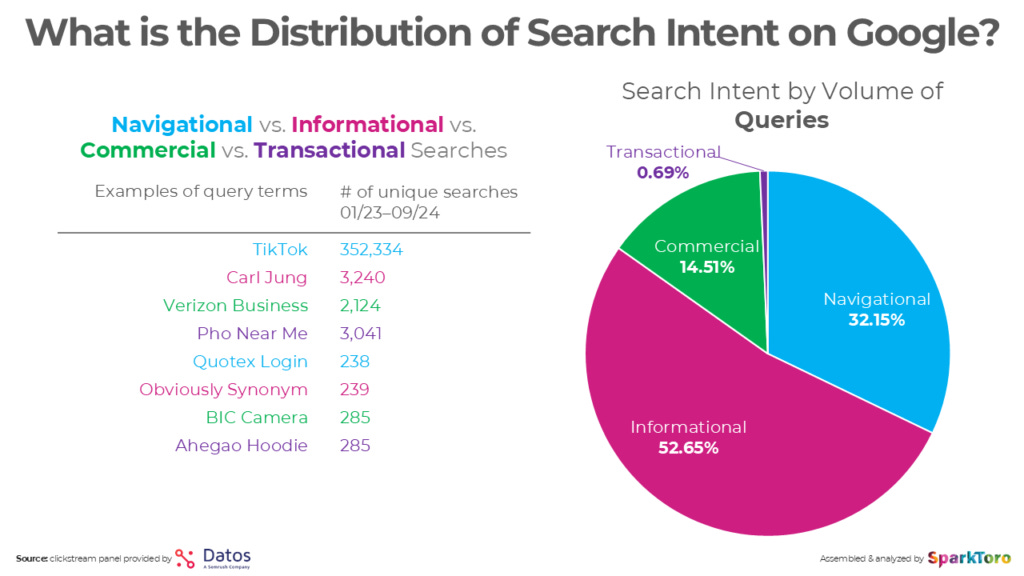

on how consumers actually search. This is a fascinating, technical analysis of query composition and volume (preview: the 60k most searched for phrases account for 75% of ALL queries!). Rand’s POV, which the data supports, is that google is less and less a place of discovery and instead is a navigational and informational portal. In other words, more and more people are searching “tiktok” instead of “best social network to grow my community” (a terrible, rudimentary example). What does this mean for brands? Two quick hits (more in the article):

Brand building matters (a lot) - you need to have people looking for you, which means you need to reach them through other channels.

Winning non-brand head terms will only get harder - a shrinking pool of non-brand volume, plus zero-click results means brands will have to get extremely creative with non-brand search. How can you stand out? How can you seed LLM’s better? How can you win on conversion rate to justify the higher CPC? Is this even a place for your brand to be?

Macro Observations:

It’s starting to feel like the world - if you are an ecommerce or digital person - is finally returning to normal. The last 4 years have produced incredible volatility and ripple effects:

2020/2021 - massive ecommerce boom due to pandemic lockdown

2022/2023 - impossible comps + major shifts in consumer preferences (travel, in-person)

In the second half of 2024, ecommerce spend as a % of total US retail spend finally surpassed the previous peak set in 2020. Further, overall ecommerce growth rates are now printing consistently positive (and growing).

Two charts below highlighting this:

There is a TON more to unpack here (i.e. the role major retailers like AMZN, WMT are playing, grocery, etc). But at a minimum, I look forward to a world of slightly more normal comps :).

Reading:

Present Brand as CAPEX, performance as OPEX: Grace Kite (the goat), has a great POV on how to have better conversations with finance. Brand media is an investment, that pays off over time, and should be considered CAPEX. Whereas performance media is more similar to OPEX and managing it should be about finding the right floor. I also love the idea presented around delivering your post year-end ROI analysis to finance - what worked, what didn’t, etc. to help build trust.

The Best Consumer Trends Report I’ve Read this Year: Imo, a report like this should be fun to read, and this one was. Fascinating data on tiktok shops, alochol consumption/preferences, gen z loyalty in beauty and more.

A Spicy Take On The (rough) State of Marketing Orgs: The author breaks down something we have been tracking, which is the fragmentation of the CMO role (into 3,4,5 different roles), and as a result, the overall and flawed fragmentation of marketing. The downstream impact of this is strategy myopia - and high efficiency but weak effectiveness. I think the reunification of marketing (think ALL 4 P’s together) is a critical investment area for CEO’s in the next 1-2 years.

Retail Brand Performance Data Shows Continued Trend of Haves/Have Nots - Lululemon up 8-9%, Under Armour down 8-9%. Yes, some categories are hurting more than others, but that doesn’t tell the whole story. Certain brands are just dominating with consumers who are making more tradeoffs & being more selective. In 2025, every single brand needs to be focused on winning at this tradeoff point. Every friction point and assumption needs to come under scrutiny (especially your retail channel strategy 👀). How do you make your brand THE choice, not just a choice?